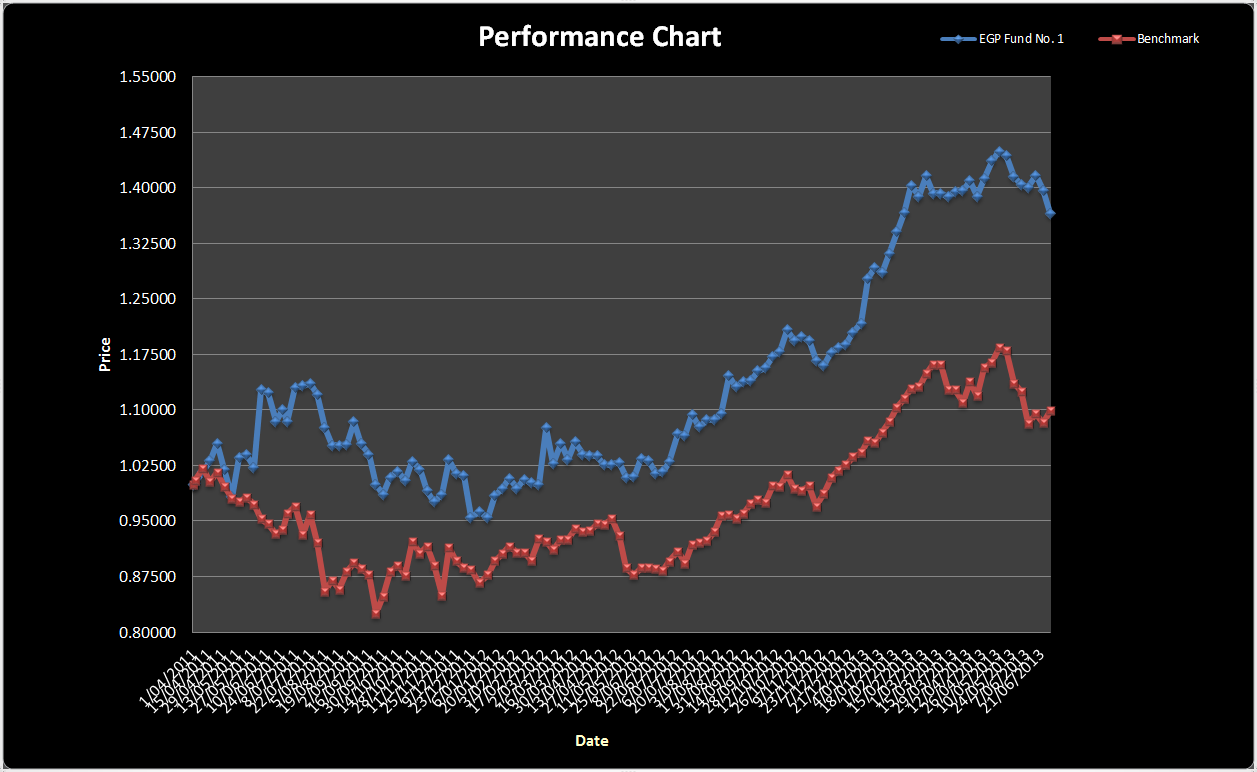

The end of financial year is upon us. Holders will find our FY2013 update here (.pdf). For people preferring a visual representation of how things are going, I’ve put that here EGP is the blue line, the ASX200 (Total Return) is red:

{kind=link}

There has been much concern about the performance of China in the news over the last few weeks, and to be sure, a major problem there would cause issues for Australia, for China is our largest trading partner (by a wide margin). But times of great uncertainty inevitably create the best opportunities. We invest with a long term time-frame and I am sure China will experience recessions, as will Australia (our current 21 year recession free run cannot last), but there are great opportunities now and always will be, regardless of economic ups and downs.

Japan has been economically stagnant for over 20 years and still represent our second largest trading partner with two-way trade totalling nearly $67 billion (.pdf) and growing at 5 or 6% per annum over the last 5 years. To put potential future growth prospects in perspective, two-way trade between Australia and India is expected to double to $40 billion by 2015. This implies about 25% annualised growth, if that rate (or anything close to it) holds for a few years, it appears likely India would reach the status of our second biggest trading partner before 2020. That would seem to be $50 billion or so of annualised export growth apparent in just the growth in our 4th largest trading partner over the next 7 or 8 years. Even if growth in our export relationship with China stagnates to the 5% levels we’ve experienced with Japan lately, given we had a $117 billion (.pdf) 2012 two-way trade, 5% growth until 2020 would still generate over $50 billion in annualised two-way trade growth by 2020.

There is also the not insignificant fact that Australia will be ‘switching on’ several major LNG projects over this same period. Although I see lots of doom and gloom about how gas prices will be affected, the fact remains that these projects will cause a meaningful jump in Australian terms-of-trade, taxation revenues etc. The ‘build’ period for these projects supported Australia through the GFC and its aftermath, but the real payoff is the production period.

Obviously there also exists the possibility that our export relationship with China not only slows but reverses; obviously this would be much more difficult to weather than the ‘moderation of growth’ scenario. I would just urge everyone to consider the range of possible scenarios and the range from mild Australian recession to absolute Australian economic disaster should not eat up too much room on your spectrum of near-term probabilities.

I don’t mean to demonstrate a Panglossian world-view, but while the breakneck export growth recently was clearly unsustainable, even with a meaningful moderation, there still seems plenty to indicate Australia’s best years are in the windscreen and not the rear-view mirror – Tony Hansen 30/06/13

|

|

Apr 1st 2011 |

Jan 1st 2013 |

Current Price |

Current Period |

Since Inception |

|

EGP Fund No. 1 |

1.00000 |

1.21730 |

1.33220*1 |

12.18%*2 |

36.55%*2 |

|

35632.05 |

37134.53 |

39163.27 |

5.46% |

9.91% |

EGP Fund No. 1 Pty Ltd. Up by 12.18%, leading the benchmark by 6.72% since January 1st. Since inception, EGP Fund No. 1 Pty Ltd is Up by 33.22%, leading the benchmark by 26.64% all-time (April 1st 2011)

*1 after 31May 2013 dividend of 2.333 cents per share plus 1 cent per share Franking Credit

*2 calculated based on dividends reinvested