I haven’t prepared a blog relating to a specific EGP investment this month. January has been in part some travel through Spain & Portugal and in the second half, mostly preparation for the upcoming reporting season in February. Instead of writing about a stock, I thought I’d sit at the keyboard and freestyle; let us see how it goes…

First thing that comes to mind, in part because the recently updated Hansen Family NTA calculation sits under my left hand as I type is wealth creation.

I deliver to Mrs Hansen twice a year an ‘NTA’ calculation that lets her know where we stand financially as I am primarily responsible for family finances. The calculation incudes all appreciating assets (Home, Superannuation, Cash & EGP holding) and subtracts any liabilities (a line of credit we keep and the previous month’s credit card expenditures if they’ve not yet been repaid). It ignores depreciating assets (cars, home contents etc.) as they are detractors from wealth in my view.

In doing this, I have been appreciating our family home at 4% each year and as a consequence, it is probably carried between 10 and 20% below what we could sell it for, given the booming Sydney housing market. I have an inkling that if I use the 4% for 2018 and 2019, that it will probably be very close to back near par and I prefer conservatism in any case.

| Year | EGP Results | Percentage Change in Hansen NTA | Percentage Change in ASX 200 (TR) | Relative Results |

| 2008 | (-17.89%) | (-38.44%) | 20.55% | |

| 2009 | 42.53% | 37.03% | 5.50% | |

| 2010 | 14.03% | 1.57% | 12.46% | |

| 2011 | (-3.75%) | 1.46% | (-10.54%) | 12.00% |

| 2012 | 26.47% | 26.12% | 20.26% | 5.86% |

| 2013 | 34.97% | 34.60% | 20.20% | 14.40% |

| 2014 | 3.71% | 6.22% | 5.61% | 0.61% |

| 2015 | 14.69% | 13.61% | 2.60% | 11.01% |

| 2016 | 29.02% | 36.82% | 11.76% | 25.06% |

| 2017 | 12.03% | 13.84% | 11.80% | 2.04% |

| Average | 15.76% | 4.14% | 11.62% |

To anyone trying to create wealth, something like the tracking I do above is very useful, the saying “What gets measured gets done” is one that’s been very important to me in my personal and professional lives.

Depending on your stage in life, the targets you set yourself will vary. For example, if you were 25 years old with only say $50k of assets, you might set yourself a pure dollar target, say growth to $75k within a year, you can control the outcome a lot more with savings when the balance is small. When you’re perhaps 50 years old with $1m in assets, you might set yourself an annual growth target of 10% annually, which would ensure at least $4m in assets by retirement age and should ensure a pretty comfortable retirement. Whatever it is, like all benchmarks, they should be set in advance and reviewed for adherence without changing the target for good reasons.

The above table demonstrates a couple of things I’d like to talk about. The first is obviously the power compounding assets at a fairly high rate has. Over the preceding 10 years, through a period that includes most of the GFC; family net worth is up roughly 4.3 times. I used the ASX200TR as our personal benchmark because I knew that the majority of our wealth would eventually be spoken for by equity investments. The ASX200TR is the benchmark of choice because it is the ‘after tax’ result and the change in the family NTA is likewise a post-tax result.

The second is how closely correlated to EGP’s results our family fortunes are. This is by design; it keeps me focused on risk with virtually all our net worth sitting inside EGP. I know our unitholders like the fact that if I make a significant mistake within EGP, I will feel it worse than anyone else, they understand it keeps my nose for risk very sensitive.

I’ll explain the two years (2011 & 2016) where the family performance has the widest differences from EGP’s. In 2011, EGP only operated from April and the market was up around 3% in the first few months, personal investments that existed pre-EGP were probably up 4 or 5%, eliminating most of the gap. In early 2016, with all the talk of changes by the Turnbull Government in the way superannuation would operate, we used the “bring-forward” rule to make 3-years’ worth of after tax contributions to superannuation, utilising the line of credit I mentioned above. 27% of the 29% EGP earned that year came after the contribution and we were substantially leveraged into it at very low borrowing cost (sub 5%) is mostly why the 2016 return is juiced up.

I estimate only 2% of the 15.76% annual growth in our net worth over the past 10 years has been through savings, it has been nearly a pure story of compounding assets. The growth I freely admit was advantaged in part by utilising leverage opportunistically and quite heavily relative to our asset base in late 2008, which is why despite an asset I only increased by 4% speaking for the majority of our net worth (family home), we still generated a 42.5% gain through 2009. I have explained this period to a number of people and I should be clear, there was a lot of luck in the timing of the deployment of leveraged capital. I do not use leverage within EGP, and generally eschew its use, but when timed correctly, it can really put a rocket under returns.

The other thing that has been exercising my mind this month, mostly because the last 4 days of our time in Spain was spent in Barcelona (the largest city in Catalonia) is the continuing trend towards separatism in politics; the last few years feel like there’s been an increase in this activity. Scotland’s referendum was only a few years back and their failed vote scarcely quieted the movements. Then the Brexit vote was successful and seems to have stiffened the spines of a number of other movements.

Obviously if we look back far enough, we see such matters pop up occasionally. Basque nationalism has bubbled away intermittently for as long as I can remember. In Quebec, there was an independence vote about 20 years back, Western Australia and Texas have occasional secessionist rumblings too. It is not uncommon, but still ‘feels’ heightened at present.

Like most areas of politics, I have views about separatism and secession that traverse the political spectrum. For example, I thought the Scottish independence vote was foolish and said at the time were I Scottish I would have voted no. There are enormous financial benefits Scots receive as part of the UK and transfer payments go only in one direction in that relationship (toward Scotland). I almost wanted it to succeed so that the supporters would see what a mistake they’d made.

My view on Brexit was very different. With the horrendous bureaucratic morass operating out of Brussels and Strasbourg, the massive cost to the UK to support a group of oxygen thieves that add a value that is measured as a tiny fraction of their cost seemed foolish. The threats emanating from those same places about how difficult they would make it in the event of Brexit succeeding would have only strengthened my decision to vote leave (had I been eligible to vote).

I would have tended lent to a low conviction support of Catalonia remaining part of Spain initially, despite the financial benefits of having Catalonia in Spain flowing more to Spain than Catalonia. The reason is that the complication of such a small country (independent Catalunya would have a population of circa 7 million) would likely outweigh the benefits gained. It is important however in a functioning democracy to have free and fair votes on matters of importance to the people.

The minute the Spanish Government sent in jack-booted thugs to crush the independence vote, any leaning I would have had as a Catalonian to remaining in Spain was eliminated. Thuggery cannot be tolerated from the people you elect to rule, except against an invading force. If leaders lack the ability to articulate the importance of a policy and resort to violence to enforce it, then they lose my support for their authority to rule. The primary (in my view) reason American independence was successful is because the founding fathers and other leaders were an inordinately articulate group who clearly explained the reasons why independence should be pursued.

If a substantial majority of citizens want something, they should get it. I would tend to want decisions about secession to be very clear majorities; I think at least a 10% (requiring a 55/45 preference) margin should be required (which incidentally would have seen Brexit fail).

Given the modern interconnectedness of the world and the very advanced weaponry available, the threat of significant global conflict has also declined so as to be almost non-existent. My personal take on this is that the conquest impulses of man have mostly been sated by the global spread of capitalism. Rather than prove dominance by armed conquest, man is inclined to pursue Business Empire building instead. This being the case, the construction of mega-countries with large populations and large standing armies as a means of self-protection is largely unnecessary. Communication being what it is, alliances could be cobbled together in a matter of hours now too.

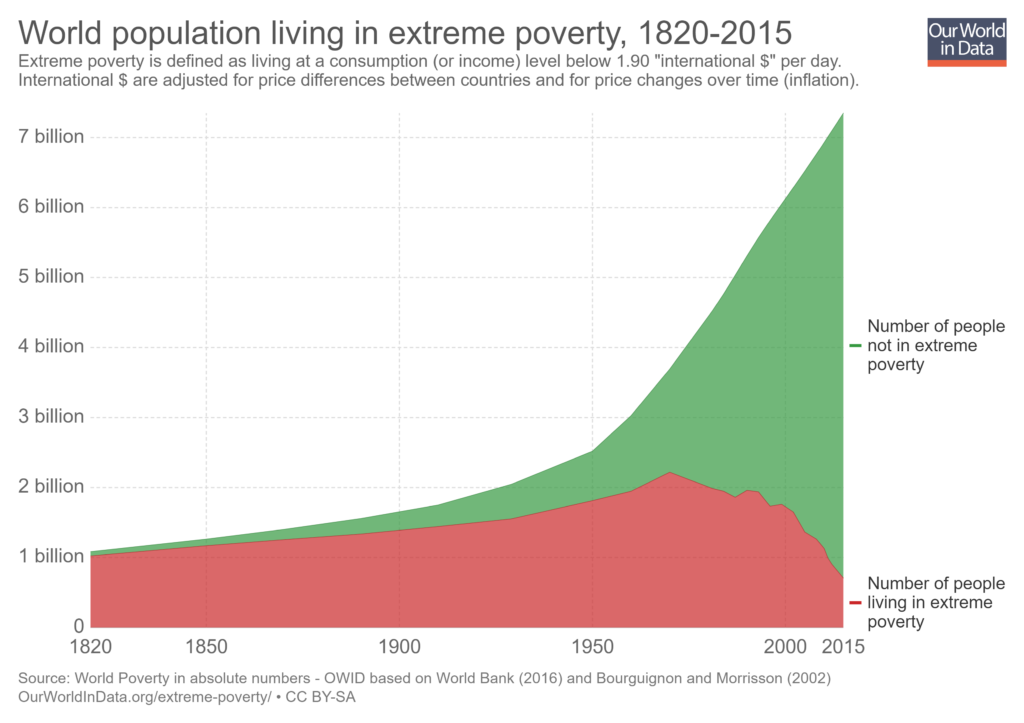

Therefore, to my view, the only downside threat of any relevance to any type of secession is the threat of protectionist behaviours in retaliation. With the benefits of free-trade obvious to any remotely fair-minded individual observe the graphic below (as an aside, if you’re ever feeling despondent about the direction of the world, 30 minutes navigating around www.ourworldindata.org should sort you out. The world is improving at an astonishing pace):

Given the shape of that graph, anyone engaging in virtually any type of protectionism is an idiot. We need to remember our Frédéric Bastiat “By virtue of exchange, one man’s prosperity is beneficial to all others”. If your primary concern is the greatest good for the greatest number, virtually any type of protectionism is unacceptable. If we can continue to expand free trade globally, sometime in the 2030’s, extreme poverty globally should be virtually eliminated for the first time in human history. Since 1970 (less than 50 years ago) the proportion of global population living in extreme poverty has declined from 60.2% to 9.6%.

My point is that breaking countries up into smaller countries shouldn’t have nearly the same risks it might have years ago. In fact, done correctly, it has the potential to substantially increase innovation globally as smaller countries can pursue diverse policies around matters such as economic, immigration, innovation, environmental, social and so on. Such a path of action serves two interesting ends in my view.

Firstly, with the much greater variety of different policy being attempted, Countries that observed a particularly successful system in another country would be able to drift in that direction and this would be easier if a smaller number of voters needed to be convinced. In much the same way the United States has the benefit (due to substantial state autonomy) of the trialling of a variety of different tax schemes, planning policies, drug, economic and environmental policies, countries would be able to do this, effectively competing to attract the best and brightest with the most widely attractive systems.

Secondly, over time, with global travel ever increasing, these smaller countries over time would sort themselves into likeminded groups. A variety of immigration and economic policies would allow people to sort themselves into groups with similar goals and preferences. Persons finding policies disagreeable would leave and vice versa.

There would be a natural population drift toward this economic opportunity. It should surprise no one that the 5 US States with the fastest growing populations over the past 10 years (Nevada, Arizona, Utah, Idaho & Texas) also have GDP growth rates in the top 10 over the same period.

There is one last thing that has been exercising my mind for the past couple of weeks. I watched a movie on the plane coming home called The Circle, I rarely watch movies, with my spare time generally spent obsessively on matters that improve EGP for the most part, but this one left me contemplative as it lay open a serious concern I have about the power of the internet giants (Google, Facebook, Amazon etc).

I should say in advance that it was no cinematic masterpiece, but the film did articulate well the threats we will face as our lives become more tangled up in algorithms. It is part of the reason I remain reluctant to enter social media platforms such as Facebook.

I do keep two social media accounts; the first is Twitter, which I mainly use as a newsfeed (and to enjoy the hilarious hand-wringing of people about the latest social justice outrage). The other is LinkedIn, which is probably a holdover from last time I was searching for a job and was not self-employed.

The only time I ever log into my linked in account is when someone sends me a connection request. A couple of requests ago, the ‘people you may know’ section popped up. On that section was a fellow I have never met, but whose name I am familiar with because he is good friends with a fellow I am closely associated with (but am not connected to through LinkedIn). I’ve wracked my brain to figure out what algorithmic association there could have been between the two of us. I cannot come up with one, and am left suspecting a device perhaps overheard mention of the name a few times. These things disturb me, perhaps more than they should.

Like most people, I enjoy some of the efficiencies algorithms bring to our lives. Amazon’s ability to narrow down potentially interesting books based on my purchasing history and the books I’m looking at is an example. I just think we should all be wary the amount of privacy we sacrifice in the pursuit of social connectedness.

I wish you all a great 2018 and look forward to hearing from many of you over the course of the year – Tony Hansen (05/02/2018)

| August 15th 2017 | Current Price | FYTD | Annualised | |

| ..EGP CVF | 1.0000 | 1.0971 | 9.71% | 22.42% |

| Benchmark .. | 56174.93 | 60154.87 | 7.08% | 16.10% |

DISCLAIMER:

EGP Capital Pty Ltd (ABN 32 145 120 681) (EGP Capital) is the holder of AFSL #499193. None of the information provided is, or should be considered to be, general or personal financial advice. The information provided is factual information only and is not intended to imply any recommendation or opinion about a financial product. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should consider seeking your own independent financial advice before making any financial or investment decisions. The information provided in this presentation is believed to be accurate at the time of writing. None of EGP Capital, Fundhost or their related entities nor their respective officers and agents accepts responsibility for any inaccuracy in, or any actions taken in reliance upon, that information. The EGP Concentrated Value Fund (ARSN 619879631) (Fund) discussed in this report is offered via a Product Disclosure Statement (PDS) which contains all the details of the offer. The Fund PDS is issued by Fundhost Limited (AFSL 233045) as responsible entity for the Fund. Before making any decision to make or hold any investment in a Fund you should consider the PDS in full. The PDS will be made available by contacting EGP Capital (info@egpcapital.com.au). Investment returns are not guaranteed. Past performance is not an indicator of future performance.

The recent issue of the Economist had an interesting piece about the future of war. I for one hope that there will never be another one. I tend agree with a lot of what you’ve said. I’m reading a book called Homo Deus which is very interesting and highly engaging, and also echoes some of the thoughts you’ve written here. As always, thanks for the update.

Homo Deus is a top 10 all time book for me. As is Sapiens, which is also by Harari. I tend to fall on the optomistic side of the spectrum… – Tony

I’ll be forwarding the family NTA content of this post to my better half. I’ve been doing something similar for the past few years and she thinks I’m the only one obsessive enough. On a serious note I wonder how many households actually a) record and b) track net wealth on a regular basis to ensure they are meeting their goals whatever they may be. Sadly I don’t think many which in aggregate must have a telling impact on social policy.

It probably is a little obsessive, but as I said in the blog, what gets measured gets done…

It is the same reason I think a large balance isn’t necessarily needed to justify having an SMSF; there is a value in being more hands on that can override the cost. You’re more likely to add more to your retirement fund each year if you’re thinking about it more while you’re doing the administration – Tony

Tony,

Is the average punter able to access leverage (such as a margin loan) for funds like yourself? I was under the belief that banks were very careful about the stocks they give leverage and margin loans to.

It’s great to have a rocket boost, but one needs to have the engine and fuel to power the rocket. No leverage, no boost right?

Great blog as always.

Potentially not, leverage to be fair has probably added 1 or 2% to the returns we’ve experenced, so we would be going OK without it. I do not use leverage inside the fund, satisfactory returns do not require it. I keep a line of credit on a house that is otherwise paid off in case exceptional opportunities present themselves. It’s not a margin loan by the way, just a simple line of credit against our home. The very great majority of people should give margin loans a very wide berth – Tony

Wise words indeed. The Industry Super funds portray themselves to be our saviour on one hand yet prey/profit on human vulnerabilities with the other. For years I have tracked every cent that goes in and out of my accounts, convinced this was highly abnormal behaviour by all to those that I divulged. I’m pleased to see there some like minded individuals out there and a shame we are the exception rather than the rule.

Keep up the exceptional blogs Tony and to those who comment. I look forward to them at the beginning of each month.