We start with the March sales. We sold our Veris (VRS.ASX) shares this month. Veris is one of the stocks we liked to capture the infrastructure boom currently underway. It was a small investment for us though which generated a respectable return despite imperfect execution. We purchased 1,649,900 shares at an average price of 15.8c, harvested a couple of small dividends and after closing the position this month, our IRR was exactly 27%. We were too tentative with our buying (in the old fund) through May and June 2017, when we bought at prices of 12c, 12.5c & 13c. In thinly traded stocks, when the prices are clearly cheap, sometimes you need to be responsible for pushing the price up yourself. However at EGP, we generally try to buy with a light touch and in situations like this it sometimes means we don’t get all of the profits we should. The business performance of VRS has not actually met my expectations, and along with the position being too small for the fund, that’s why we eliminated the holding. If they execute on their strategy, they could well continue to see the share price rise, but we were happy to take the gains we made and move on.

We also sold our Salmat (SLM.ASX) position this month. We purchased SLM in July last year when we were offered a rare opportunity to get a decent amount of stock in a single transaction as it is a particularly difficult stock to buy on market. Subsequently, CEO Rebecca Lowdes has done an excellent job in executing SLM’s stated rationalisation strategy. They have exited the weaker businesses they were in and are now left with a respectable business and a pile of cash that speaks for more than half the capitalisation of the business. There is probably a bit more upside left in the business, given what a good job has been done so far, but they say it’s safest to ‘leave a little meat on the bone’ when you sell and we will be pleased if the buyer of our stake has nearly as good an experience as we did. At the sale price, SLM represented almost 3% of our invested capital and upon completing the sale our IRR including dividends was 139%.

We made a considerable purchase this month also in the 8.3% stake we took in the APN Regional Property Fund (APR.NSX). We have purchased this stake at slightly more than a 13% discount to Net Tangible Assets. The managers have committed to generating a liquidity event by 30 June 2018.

The exact outcome of the liquidity event could take a number of forms, but for simplicity, assuming they were able to provide a sale at NTA, and we received the cash on 30 June 2018, our IRR on the holding would be a shade over 75% (mostly due to a short holding period).

The two properties that comprise the asset are valued at a capitalisation rate of 7.85%. They have a short WALE and familiar as I am with the Newcastle office market (with the help of some EGP unitholders who operate in that space), and the relative dearth of decent quality office space, we think the asset could potentially be attractive to the right owner and could attract a sharper cap rate at sale than present valuation.

Assuming the 30 June 2018 promised liquidation dates comes and goes, we would continue to receive the quarterly payment of 2.375c that means the asset is returning us about 8.3% on our cost base while we await the outcome.

If we further assume that the liquidity event takes 6 months longer than expected and close at NTA by 31 December 2018, then we will have still earned a respectable IRR of more than 28%. We consider the risk return profile of this investment to be particularly attractive. We will likely meet with the management team in the next couple of weeks to offer any help we can to ensure a speedy and profitable resolution to the matter – Tony Hansen (04/04/2018)

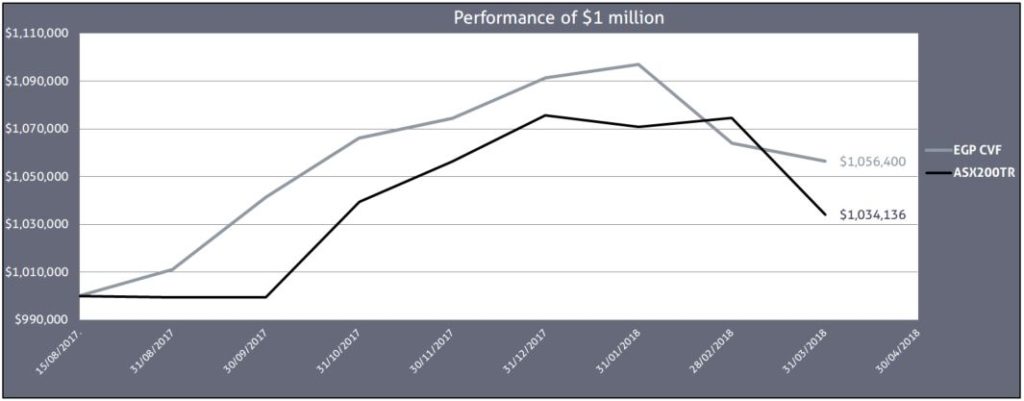

| August 15th 2017 | Current Price | FYTD | Annualised | |

| ..EGP CVF | 1.0000 | 1.0564 | 5.64% | 9.18% |

| Benchmark .. | 56174.93 | 58092.50 | 3.41% | 5.51% |

DISCLAIMER:

EGP Capital Pty Ltd (ABN 32 145 120 681) (EGP Capital) is the holder of AFSL #499193. None of the information provided is, or should be considered to be, general or personal financial advice. The information provided is factual information only and is not intended to imply any recommendation or opinion about a financial product. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should consider seeking your own independent financial advice before making any financial or investment decisions. The information provided in this presentation is believed to be accurate at the time of writing. None of EGP Capital, Fundhost or their related entities nor their respective officers and agents accepts responsibility for any inaccuracy in, or any actions taken in reliance upon, that information. The EGP Concentrated Value Fund (ARSN 619879631) (Fund) discussed in this report is offered via a Product Disclosure Statement (PDS) which contains all the details of the offer. The Fund PDS is issued by Fundhost Limited (AFSL 233045) as responsible entity for the Fund. Before making any decision to make or hold any investment in a Fund you should consider the PDS in full. The PDS will be made available by contacting EGP Capital (info@egpcapital.com.au). Investment returns are not guaranteed. Past performance is not an indicator of future performance.

Hi Tony

I see your preferred assessment of performance is IRR. May I ask how many years of future cash flows do you use in the calculation of IRR?

All the best, Mark

We’re usually looking 5 years out Mark. We use IRR so I don’t get tempted to put the cash to work just to beat the cash rate. We target >20% at deployment and <10% at exit. So effectively if the price of an investment we purchased today with a 5 year outlook for 20% IRR rose by more than 55% tomorrow and our valuation remained unchanged, it would become a candidate for sale. It's not quite this mechanical obviously, but that is the intellectual underpinnings of what we do - Tony